The Decision Layer: For Indian D2C Brands

How we are trying to bridge the decision gap in Indian D2C brands

When we started building Ocular last year, our thesis fit on a single slide.

“The decision engine for e-commerce brands.”

That was the header of the first deck I ever pitched. It came from a frustration I kept running into one that didn’t quite make sense at first.

Before Ocular, we worked with several large D2C brands to build their internal data platforms. These weren’t scrappy outfits. They had the budget, the team, and the appetite to buy the best tools the market had to offer.

A best-in-class retention platform. A dedicated performance marketing stack. Marketplace tooling. Ops and inventory software. Every function covered, with the leader in that category.

And these tools weren’t optional they were essential. The retention team couldn’t ship without theirs. The performance team couldn’t run campaigns without theirs. Each tool sat at the centre of a function’s daily operating cadence, and that wasn’t going to change.

And yet every one of these brands eventually came to us with the same ask:

“Can you help us build something on top of all this?”

It took a while to understand why. They already owned best-in-class, and the tools were working. What more could possibly be missing?

The tool problem

The insight, when it finally landed, was simple but defining:

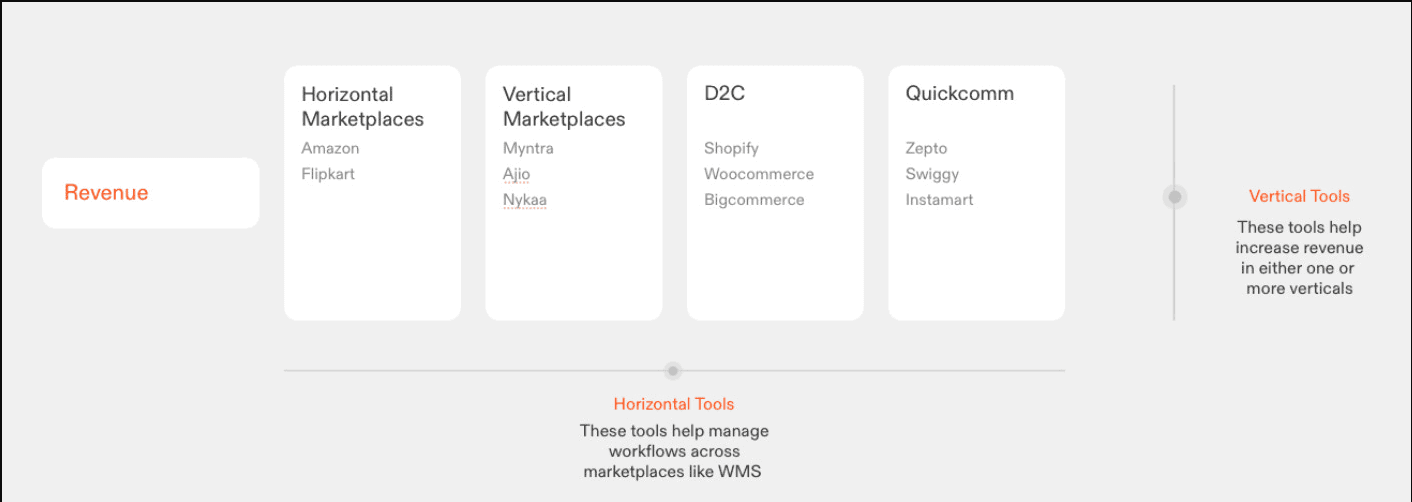

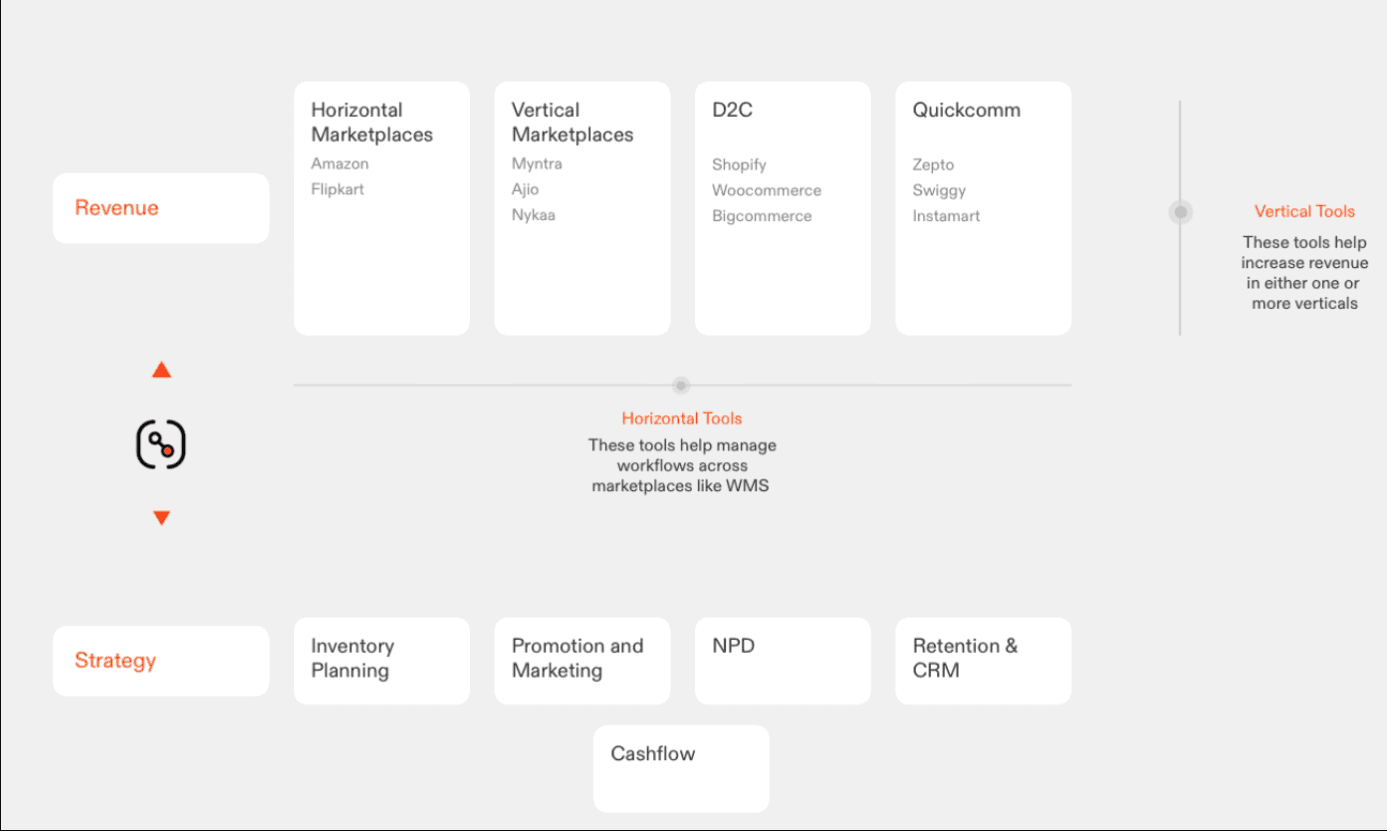

Every tool in the e-commerce stack solves a vertical or a horizontal problem.

Retention tools optimize retention. Marketplace tools optimize marketplaces. Performance marketing tools optimize spend. Each is excellent at its slice, indispensable inside that slice and essentially blind to everything outside it.

That’s fine when the question lives entirely inside one slice. “What’s our best-performing ads this week?” is a retention question. “What’s our TACoS trending toward?” is a marketplace question. The vertical tools answer these brilliantly which is exactly why brands keep them.

But the decisions that actually run a brand don’t live inside any one slice. They cut across all of them.

What real decisions actually look like

Sit in on any brand operator’s Monday meeting and the questions sound more like this:

We can fund either the new product launch or another quarter of aggressive acquisition, cash flow won’t stretch to both. Which one compounds faster?

The campaign goes live in three weeks. Will inventory hold to peak, or do we throttle creative midway and waste the brief?

We’re 8% behind plan with two months left in the quarter. Which lever moves the number fastest without breaking next quarter’s setup?

Three competitors just dropped price by 8% on our category. Hold, match, or counter.

Marketing is forecasting a 35% Q4 lift. Does ops believe it? Does finance? When the numbers don’t agree, whose forecast does the brand actually run on?

Our marketplace business is growing 40% faster than DTC, but unit economics are four points worse. At what point do we cap it and what does the cap cost us this year?

None of these is a dashboard query. Each one threads through three or four different platforms and then has to be reconciled with data that doesn’t live inside any vendor’s tool: your P&L, your supply chain, your roadmap, your competitive intel, your priorities for the quarter.

The two choice

Brands serious about answering these questions had, until now, two paths in front of them.

Build it internally. Hire data engineers, stand up a warehouse, pipe every tool into it, model the data, build dashboards. This works. Done well, it produces deep, owned capability and for brands with the scale, capital, and data culture for it, that’s often the right call. The price is months and several $$ before anything ships, plus a team to keep it alive after.

Hire consultants. Bring in firms like ours (yes, we are that firm as well) to build the platform for you. Faster than internal, and you don’t have to hire data engineers and analysts in a market that’s punishing to hire in. The trade-off is that what gets built is still a bespoke system yours to operate once the consultants leave, and built without the benefit of what every other brand has already figured out.

Both paths are real, and both produce something that works. What kept striking us is that the layer itself, the structural piece between the vertical tools and brand-level decisions is identical across brands. The data is different, the priorities are different, the outputs are different. But every serious brand ends up rebuilding the same scaffolding from zero.

That’s not a per-brand problem. That’s a product.

What we’re building

So we flipped the model. Instead of building one data platform per brand, we’re building the layer that sits on top of every brand’s existing stack.

The vertical tools don’t go anywhere. They stay exactly where they are, doing exactly what they do because they’re essential to how each function operates. Ocular doesn’t replace them. It sits above them, pulling in their signals, layering in the cross-functional inputs (cash flow, inventory, NPD, targets, competitor data), and unifying everything into one place.

A single source of truth built not for one vertical, but for the brand.

Why this is the bet

The way I see it, e-commerce has spent the last decade getting really good at vertical optimization. We’ve squeezed every last point of efficiency out of email flows, ad creative, listing optimization, retention curves. The vertical tools deserve credit for that, and they’ll keep delivering it.

The next decade is about brand-level optimization. It’s about answering the harder, slower, more important questions: where to deploy capital, what to launch next, when to pull back, how to compound.

Those decisions need a layer.

Ocular is that layer.